Output is projected to grow at 3.6% in 2025 and 3.4% in 2026, before increasing by 4.0% in 2027. Higher tariffs will weaken exports, but the effect is expected to be relatively small and short-lived. Improved financial conditions will support private consumption and investment in 2026 and 2027, which in turn will trigger stronger imports. The decline in inflation is projected to continue. Headline inflation is expected to fall to 10% by the end of 2027, but upside risks to this projection remain significant.

Monetary policy has become more supportive in the third quarter of 2025 as the central bank started to reduce its policy rate. Lower inflation will allow further interest rate reductions in 2026 and 2027, but the tight monetary policy stance should be sustained until inflation has declined durably. The fiscal deficit is expected to narrow. Regulatory reforms to reduce barriers to entry in services sectors will be key to raise long-term growth potential, along with policy efforts to boost labour force participation and improve skills.

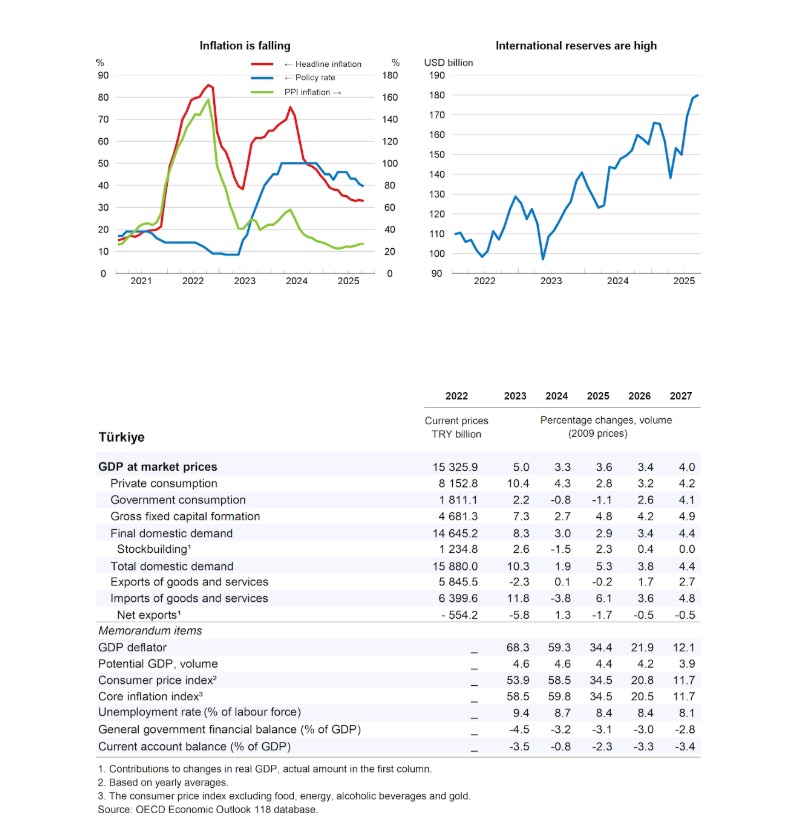

Tight financial conditions have weighed on domestic demand

Exports and imports rose by 3.9% and 6.0% year-on-year, respectively, between January and October, while industrial production increased by 3.1% year-on-year between January and August. Consumer spending remains subdued. Tight monetary and fiscal policies have contributed to disinflation over the first half of 2025, but high inflation expectations and inertia remain. Year-on-year inflation has declined to 32.9% in October 2025, from 37.9% in April 2025, while education and housing has pushed service inflation above the headline. Producer price inflation increased from 22.5% in April to 27.0% in October, partly due to higher import prices. Unemployment averaged 8.5% between July and September 2025, continuing the downward trend of the past five years. Moderate real wage increases in the first half of 2025, following a large rise in 2024, supported disinflation but weighed on consumer confidence. Business confidence has declined since March.

The United States has applied a 15% tariff rate on Türkiye’s exports since August 2025. The direct impact of this is likely to be limited as exports to the US only account for about 6% of Türkiye’s exports and 1% of GDP, but changing trade policies could affect Türkiye through a slowdown in European demand.Source: Central Bank of Turkey; Bank for International Settlements; and International Monetary Fund.

The policy mix will remain mildly contractionary

The fiscal deficit is assumed to decline from 3.1% of GDP in 2025 to 2.8% in 2027, in line with the Medium-Term Programme. This consolidation will be driven by efforts to broaden the tax base and tackle informality. The central bank’s policy rate is projected to decrease from 40.5% in the third quarter of 2025 to 25% at the end of 2026 and 17% at the end of 2027 amid declining inflation. Nevertheless, the real interest rate will remain positive and high, keeping monetary policy restrictive.

Domestic demand will pick up and disinflation will continue

Domestic demand is expected to pick up as real wages continue to recover and confidence improves. In 2025, annual GDP growth benefited from a strong build-up of inventories in the second quarter and is expected to reach 3.6%. Quarterly growth will strengthen steadily over 2026 and 2027, with annual GDP growth reaching 3.4% in 2026 and 4.0% in 2027. Strong domestic demand will lead to a surge in imports, and an increased but moderate current account deficit. Unemployment will continue to decline slowly, reaching 8% at the end of 2027. Disinflation is set to continue, with headline inflation expected to reach 10% by the end of 2027. However, inflation may surprise on the upside, particularly if monetary policy normalisation is premature. Prolonged political uncertainty could bring pressure on the exchange rate and foreign reserves, potentially resulting in higher interest rates and borrowing costs, while business and consumer confidence could also suffer.

Structural reforms can sustain long-term growth

Continuing the stabilisation of the economy will remain the policy priority until inflation is firmly converging towards the target. Current fiscal consolidation efforts will support this, but risks from contingent liabilities should continue to be monitored closely. Ensuring a stable and predictable regulatory policy framework will be key to improve investor sentiment and attract more international investment. Simplifying insolvency regulations for small and medium enterprises could foster capital reallocation towards better-performing businesses. This could be supported by more flexibility in permanent labour contracts and a cautious approach to future minimum wage increases in order to promote formal job creation, which is particularly relevant among smaller firms. Boosting female labour force participation, improving skills and reducing regulatory barriers to entry in services can further support ongoing efforts to raise long-term growth potential.